August 2024 - San Diego Real Estate Market Update

Since the Spring of 2022, when mortgage interest rates began their climb, the story about the real estate market has remained more or less the same – because interest rates are high, there is a lock-in effect preventing homeowners from selling, and though affordability is challenging for homebuyers, inventory of homes for sale is so low that supply and demand are out of sync and prices are rising. And while it wouldn’t quite be true to say the landscape today looks different from that, we are starting to see changes that will lead the market in a different direction… Finally.

When the pandemic hit, the economy crashed and the U.S. government needed to act to prevent a wider financial disaster. They did a great job of that, using stimulus measures. Grants and loans to business owners got people back to work, stimulus checks and consumer habit shifts padded people's bank accounts, and the Federal Reserve’s interest rate drop spurred consumer spending. No one is saying there isn’t plenty to criticize about these measures, but they did serve the intended purpose in the short term. The housing market in particular benefitted from these stimulus measures – mortgage rates were at rock bottom and people were eager to move. As a result, home prices skyrocketed. The prices of everything else also skyrocketed, between rabid spending and supply chain issues, inflation spiraled out of control to a 4-decade high.

The Fed did what the Fed does, they used their power over interest rates, in this case, to restrict spending, and the real estate market was hit hard and fast. As mortgage rates skyrocketed, 90% of homeowners had a rate below 4%. As rates climbed to 6%, then 8%, homeowners simply couldn’t afford to move, so if they didn’t absolutely have to, they didn’t. As painful as this process was, it was exactly what the Fed intended – they needed to tame inflation and the housing market was a huge contributor to overall frothy price growth.

Now, inflation is back down to very near the Fed’s 2% target, but we’ve also started to see an uptick in unemployment, signaling that the tightening policy the Fed has been employing risks going too far if they don’t start lowering rates soon. Fed chair Jerome Powell has signaled that a September rate cut is all but guaranteed – and now the question is, how much will the Fed cut rates, and how quickly?

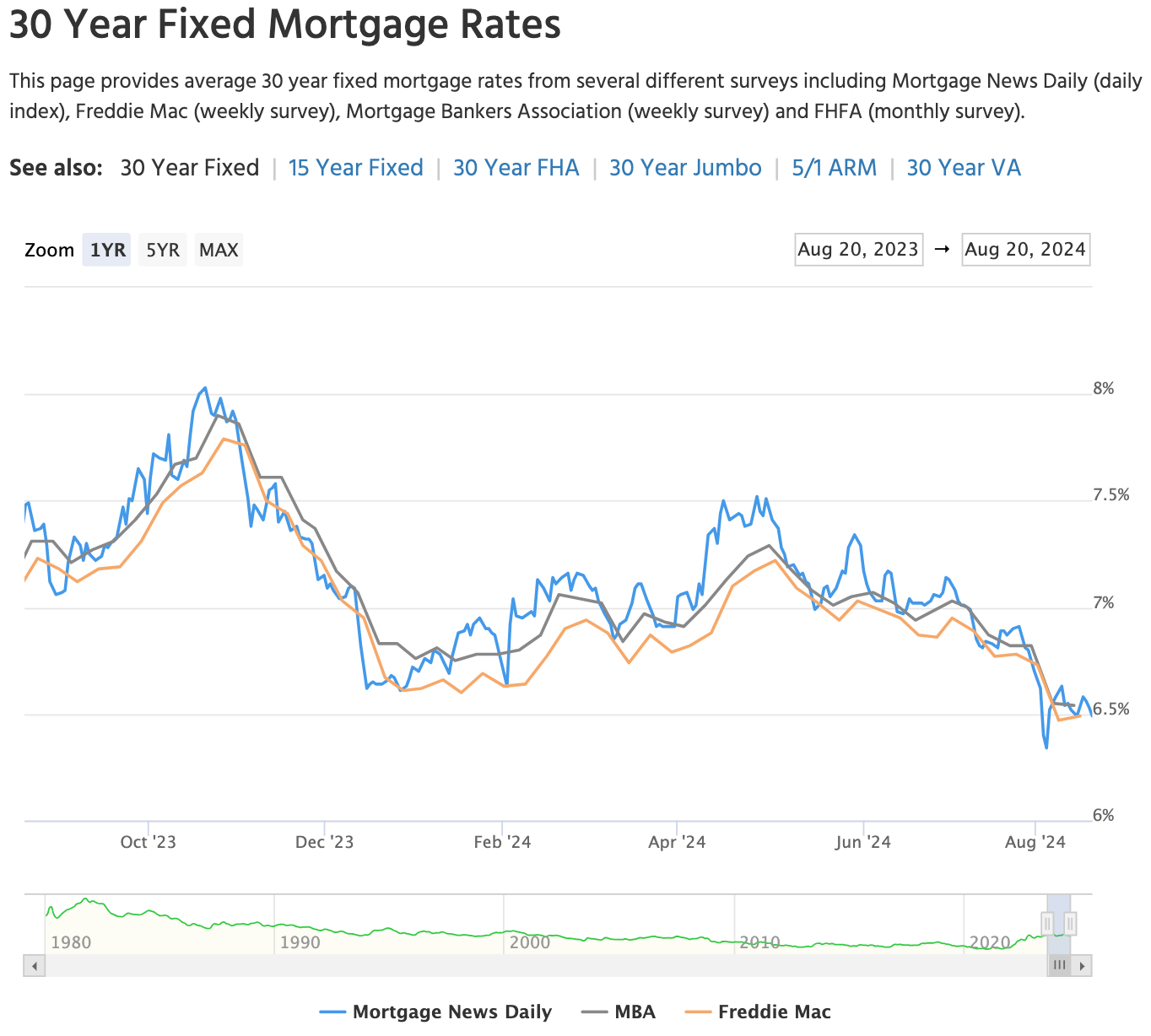

Mortgage Interest Rates

The market has probably already priced in the upcoming September rate cut as mortgage rates have fallen to around 6.5% from last month’s floor of 6.8%. Because of that, it remains to be seen whether a September Fed rate cut will greatly impact mortgage rates in the short term. Ultimately, though, we should expect to see rates trending downward for the remainder of this year and through 2025. That being said, rates will likely inch down slowly to prevent a huge spike in demand that would cause prices to spike again. If we did see a large drop in rates all at once, buyers would flood the market and we’d see lines for open houses and rabid bidding wars make a return – this is what got us into trouble in the first place, so the Fed is going to be working to avoid this.

Home Prices

Home prices have flattened and have even fallen slightly in some areas, however, there is still a healthy net gain year-over-year. While median home prices have fallen, the average price per square foot of sold properties is fairly flat. This indicates that a larger share of the homes that are currently selling fall below the median price and that fewer more expensive homes are selling – but prices are not actually losing a ton of steam.

Typically, in years when interest rates are falling, home price growth is slower. This is because falling interest rates are a sign that the economy is struggling. Conversely, when interest rates are rising, home prices often rise more quickly as rising interest rates are a sign of an overheated economy. Whether this trend holds true in the coming months and years will be dependent upon whether the Fed is able to accomplish a so-called “soft landing,” defined by taming inflation without triggering a recession. If we don’t experience a recession, we will likely see lower interest rates cause faster price growth as they entice more buyers back into the market. If we do see a recession coupled with a slow pace of interest rate decreases, prices will likely stay more level – but don’t anticipate major declines. Extremely low inventory is a chronic problem and without a glut of inventory, major price declines are off the table. There is no reason to believe there is a major inventory surge anywhere on the horizon as foreclosure rates are extremely low and homeowners are both extremely well-qualified for the mortgages they hold and are equity-rich.

Real Estate Sales Activity and Demand for Homes

Demand for homes has improved slightly as mortgage rates have, too. There’s been an uptick in mortgage applications in recent weeks while pending home sales have also increased. We are headed into what is typically the slow season for home sales and with a presidential election looming, we would ordinarily expect to see that seasonal slowdown amplify. That being said, falling mortgage rates could spur more activity than typical during the fall and winter months this year. If you’re considering buying, it could be a solid strategy to take this opportunity to secure a home while prices and competition are more moderate – you can always refinance later as rates continue to fall.

Inventory of Homes for Sale

Inventory of homes for sale rose all year long, yet still remains low by historical standards. Regardless of falling mortgage rates, inventory is likely to remain level or fall through the end of the year as homeowners tend to avoid listing their properties and moving over the holidays, and homebuilders hold off due to affordability and weather challenges. That being said, if you are considering selling, this can be a great time of year to list as there are fewer homes on the market to compete with – especially if we see more buyers in the market due to lower rates.

Economic Outlook

Expectations for where the economy is headed from here are suspended in mid-air right now. The economy is strong in many regards and the Fed’s mandate to accomplish a soft landing has thus far been effective. Did the Fed wait too long to lower rates? Is unemployment going to get worse? Are we headed for a recession? The odds are leaning toward no, it looks like we’re going to avoid recessionary times for now. But, while banks and economists are saying the odds are low now, any new financial data could increase those odds. Keep an eye on jobs data for insight into how things are going… or better yet, keep reading this newsletter each month.

In Conclusion

They say that attempting to time the market is a fool’s errand. That tends to be true, but there are arguments for why now is a good time to buy or sell, assuming you are ready to do so. Ultimately, your readiness and your goals are all that truly matter. Beyond that, relying on your trusted real estate advisor (that’s me!) to inform you about the current market, potential obstacles, and a strong strategy is the most important step you can take.

P.S. You’ve probably heard that rules have changed when it comes to how homebuyers work with real estate agents, and how commissions are paid. These rules will impact everyone differently, so your particular situation is important when understanding how they will affect you personally. If you have questions about this, reach out anytime.

Most importantly, if you have questions or concerns about your specific situation… CALL ME to help sort through them. That’s why we get up in the morning - not just to sell homes, but to serve our clients.

As always, we will be here to continue to provide you with updates about the housing market and answer any and all of your questions. Feel free to reach out to us anytime.

HOMEOWNER RESOURCES:

FUTURE HOME BUYER RESOURCES:

Say Hello

Get in Touch With Us

301 Santa Fe Drive Ste B, Encinitas, CA, 92024